Page 8 - MWC 10-5-2023s

P. 8

The Midwest Cattleman · October 5, 2023 · P8

MARKET REPORT

Live Cattle Feeder Cattle Daily

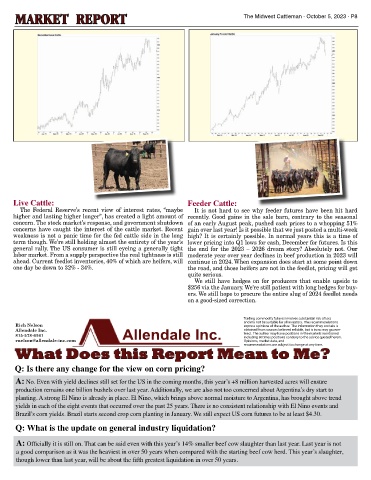

Live Cattle: Feeder Cattle:

The Federal Reserve’s recent view of interest rates, “maybe It is not hard to see why feeder futures have been hit hard

higher and lasting higher longer”, has created a light amount of recently. Good gains in the sale barn, contrary to the seasonal

concern. The stock market’s response, and government shutdown of an early August peak, pushed cash prices to a whopping 51%

concerns have caught the interest of the cattle market. Recent gain over last year! Is it possible that we just posted a multi-week

weakness is not a panic time for the fed cattle side in the long high? It is certainly possible. In normal years this is a time of

term though. We’re still holding almost the entirety of the year’s lower pricing into Q1 lows for cash, December for futures. Is this

general rally. The US consumer is still eyeing a generally tight the end for the 2023 – 2026 dream story? Absolutely not. Our

Live Cattle: My thoughts center around this market stabilizing now. I’ve been

Feeder Cattle: All you have to do is look at the corn market for a reason for the

labor market. From a supply perspective the real tightness is still moderate year over year declines in beef production in 2023 will

placing a bullish tilt to this market for some time now. I may need to temporarily

pull-back in feeders. If I owned a feedlot I’d be nervous to say the least. I do feel

ahead. Current feedlot inventories, 40% of which are heifers, will continue in 2024. When expansion does start at some point down

place this on “hold” for a while. The higher placements the last three months will

the feeder market has overdone it to the downside and it will be tough to break it

one day be down to 32% - 34%. the road, and those heifers are not in the feedlot, pricing will get

further. The early corn harvest has most feeder buyers in the field and I don’t think

have a negative impact on prices yet, so like they say, “All good things come to those

who wait”. I see production numbers staying over last years’ levels until at the quite serious.

they’ve really had time to concentrate on buying feeders. Let’em get caught up a

We still have hedges on for producers that enable upside to

least the end of the year. Beef shipments have been lagging last years’ levels now little and they’ll head to town.....checkbooks in hand....bulging with “corn” money.

for about a month. Two weeks ago they were 8% lower than last year. This weeks $256 via the January. We’re still patient with long hedges for buy-

This market will rally....wait and see.

report showed exports a whopping 56% lower than last year. This ain’t good. Low ers. We still hope to procure the entire slug of 2024 feedlot needs

imports and high exports have held this market up all summer. We’re starting to

lose some of that. I just can’t pull the trigger yet on long term bullish hopes. on a good-sized correction.

Trading commodity futures involves substantial risk of loss

and my not be suitable for all investors. The recommendations

Rich Nelson express opinions of the author. The information they contain is

Allendale Inc. Allendale Inc. obtained from sources believed reliable, but is in no way guaran-

815-578-6161 teed. The author may have positions in the markets mentioned

including at times positions contrary to the advice quoted herein.

rnelson@allendale-inc.com Opinions, market data, and

recommendations are subject to change at any time.

What Does this Report Mean to Me?

Q #1

Q: Is there any change for the view on corn pricing?

What do you think the price of fats will be in April 2011

Answer: It’s hard to see the forest for the trees here, but peering through the foliage I see $105.00 fats on the horizon for April. Demand is

A: No. Even with yield declines still set for the US in the coming months, this year’s +8 million harvested acres will ensure

going to have to kick in though in order to get it.

production remains one billion bushels over last year. Additionally, we are also not too concerned about Argentina’s dry start to

Q #2

planting. A strong El Nino is already in place. El Nino, which brings above normal moisture to Argentina, has brought above trend

Due to the recent break in feeders, would you be holding your fall-weaned

yields in each of the eight events that occurred over the past 25 years. There is no consistent relationship with El Nino events and

calves for a while or letting them go?

Brazil’s corn yields. Brazil starts second crop corn planting in January. We still expect US corn futures to be at least $4.30.

Answer: What ever happened to the easy questions? This will depend upon your weaning sched-

Q: What is the update on general industry liquidation?

ule and your available feed supply. I’m long term bullish the feeder market but the “reality” of

right now probably dictates letting them go. If you keep them for an extra 30 days, make sure you

A: Officially it is still on. That can be said even with this year’s 14% smaller beef cow slaughter than last year. Last year is not

minimize the grain in the ration. Grow them on good forage....”sell” $4.50 corn. If the fat market

a good comparison as it was the heaviest in over 50 years when compared with the starting beef cow herd. This year’s slaughter,

stays sluggish and corn prices don’t moderate, about the only thing you’ve got to hang your hat on

for “higher feeders” is “Hope”.

though lower than last year, will be about the fifth greatest liquidation in over 50 years.

November 6th

Auction

Lunch at 11:00 a.m.

Sale at 12:30

Sale Offering

16 - 2010 Heifer Calves Jan. - May

16 - Breeding Bulls 7 to 18 months RH Standard Lad 0313

16 - Spring Calving Bred Females Solid As A Rock Sire Group

16 - Spring Calving Black Females Reynolds Herefords

Bred to Hereford Bulls

8 - Fall Calving Pairs 1071 County Road 1231

6 - Show Steer Prospects

Both Horned & Polled Offered Huntsville, MO 65259

Home: 660-277-3679 • Matt: 660-676-3788

November 5, 2010 Sale offerings on

Display 3:00 P.M.

CHB Dinner at 6:00 P.M. • Barb: 660-676-4788

Call or E-Mail for Catalog Email: reynoldscattle@cvalley.net