Page 8 - MWC 02-04-2021s

P. 8

The Midwest Cattleman · February 4, 2021 · P8

MARKET REPORT

Live Cattle Feeder Cattle Daily

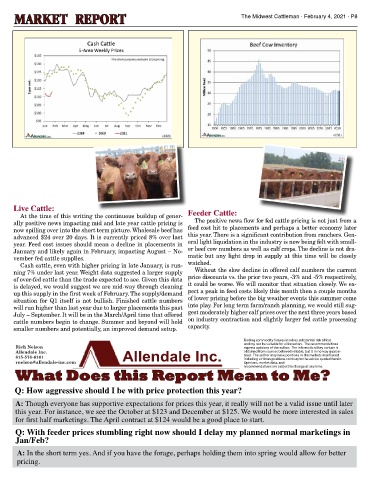

Live Cattle:

At the time of this writing the continuous buildup of gener- Feeder Cattle:

ally positive news impacting mid and late year cattle pricing is The positive news flow for fed cattle pricing is not just from a

now spilling over into the short term picture. Wholesale beef has feed cost hit to placements and perhaps a better economy later

advanced $24 over 20 days. It is currently priced 8% over last this year. There is a significant contribution from ranchers. Gen-

year. Feed cost issues should mean a decline in placements in eral light liquidation in the industry is now being felt with small-

January and likely again in February, impacting August – No- er beef cow numbers as well as calf crops. The decline is not dra-

vember fed cattle supplies. matic but any light drop in supply at this time will be closely

Cash cattle, even with higher pricing in late January, is run- watched.

Without the slow decline in offered calf numbers the current

ning 7% under last year. Weight data suggested a larger supply Feeder Cattle: All you have to do is look at the corn market for a reason for the

Live Cattle: My thoughts center around this market stabilizing now. I’ve been

of over-fed cattle than the trade expected to see. Given this data price discounts vs. the prior two years, -3% and -5% respectively,

pull-back in feeders. If I owned a feedlot I’d be nervous to say the least. I do feel

placing a bullish tilt to this market for some time now. I may need to temporarily

is delayed, we would suggest we are mid-way through cleaning it could be worse. We will monitor that situation closely. We ex-

place this on “hold” for a while. The higher placements the last three months will

the feeder market has overdone it to the downside and it will be tough to break it

have a negative impact on prices yet, so like they say, “All good things come to those pect a peak in feed costs likely this month then a couple months

up this supply in the first week of February. The supply/demand further. The early corn harvest has most feeder buyers in the field and I don’t think

who wait”. I see production numbers staying over last years’ levels until at the

they’ve really had time to concentrate on buying feeders. Let’em get caught up a

situation for Q1 itself is not bullish. Finished cattle numbers of lower pricing before the big weather events this summer come

least the end of the year. Beef shipments have been lagging last years’ levels now

little and they’ll head to town.....checkbooks in hand....bulging with “corn” money.

will run higher than last year due to larger placements this past into play. For long term farm/ranch planning, we would still sug-

This market will rally....wait and see.

for about a month. Two weeks ago they were 8% lower than last year. This weeks

report showed exports a whopping 56% lower than last year. This ain’t good. Low gest moderately higher calf prices over the next three years based

July – September. It will be in the March/April time that offered

imports and high exports have held this market up all summer. We’re starting to on industry contraction and slightly larger fed cattle processing

cattle numbers begin to change. Summer and beyond will hold

lose some of that. I just can’t pull the trigger yet on long term bullish hopes.

smaller numbers and potentially, an improved demand setup. capacity.

Trading commodity futures involves substantial risk of loss

and my not be suitable for all investors. The recommendations

Rich Nelson express opinions of the author. The information they contain is

Allendale Inc. Allendale Inc. obtained from sources believed reliable, but is in no way guaran-

815-578-6161 teed. The author may have positions in the markets mentioned

including at times positions contrary to the advice quoted herein.

rnelson@allendale-inc.com Opinions, market data, and

recommendations are subject to change at any time.

What Does this Report Mean to Me?

Q #1

Q: How aggressive should I be with price protection this year?

What do you think the price of fats will be in April 2011

Answer: It’s hard to see the forest for the trees here, but peering through the foliage I see $105.00 fats on the horizon for April. Demand is

A: Though everyone has supportive expectations for prices this year, it really will not be a valid issue until later

going to have to kick in though in order to get it.

this year. For instance, we see the October at $123 and December at $125. We would be more interested in sales

Q #2

for first half marketings. The April contract at $124 would be a good place to start.

Due to the recent break in feeders, would you be holding your fall-weaned

Q: With feeder prices stumbling right now should I delay my planned normal marketings in

calves for a while or letting them go?

Jan/Feb?

Answer: What ever happened to the easy questions? This will depend upon your weaning sched-

ule and your available feed supply. I’m long term bullish the feeder market but the “reality” of

A: In the short term yes. And if you have the forage, perhaps holding them into spring would allow for better

right now probably dictates letting them go. If you keep them for an extra 30 days, make sure you

pricing.

minimize the grain in the ration. Grow them on good forage....”sell” $4.50 corn. If the fat market

stays sluggish and corn prices don’t moderate, about the only thing you’ve got to hang your hat on

for “higher feeders” is “Hope”.

November 6th

Auction

Lunch at 11:00 a.m.

Sale at 12:30

Sale Offering

16 - 2010 Heifer Calves Jan. - May

16 - Breeding Bulls 7 to 18 months RH Standard Lad 0313

16 - Spring Calving Bred Females Solid As A Rock Sire Group

16 - Spring Calving Black Females Reynolds Herefords

Bred to Hereford Bulls

8 - Fall Calving Pairs 1071 County Road 1231

6 - Show Steer Prospects

Both Horned & Polled Offered Huntsville, MO 65259

Home: 660-277-3679 • Matt: 660-676-3788

November 5, 2010 Sale offerings on

Display 3:00 P.M.

CHB Dinner at 6:00 P.M. • Barb: 660-676-4788

Call or E-Mail for Catalog Email: reynoldscattle@cvalley.net